.png)

More than being known for Machu Picchu, Peru is the sixth largest economy in Latin America. With a population of 33 million people — 72.3% living in urban areas and 27.7% in rural areas — the country relies on both public and private services to provide healthcare access.

Overall, the country allocates 5.5% of its US$289.22 billion GDP to the health sector. In 2025, Peru’s health budget is S/251.8 billion — approximately R$186 billion — a value 3% higher than in 2024 and 194% higher compared to ten years ago.

This amount is intended to support the functioning of the entire sector, but especially the five main institutions that form the country’s mixed and fragmented system:

- Ministerio de Salud (MINSA);

- Seguro Integral de Salud (SIS), under MINSA and focused on the poorest population (60% of the population);

- EsSalud, the contributory system for formal workers (30% of the population);

- Programs for the armed forces and police (5%);

- Private sector, supplemental insurance, and individual care.

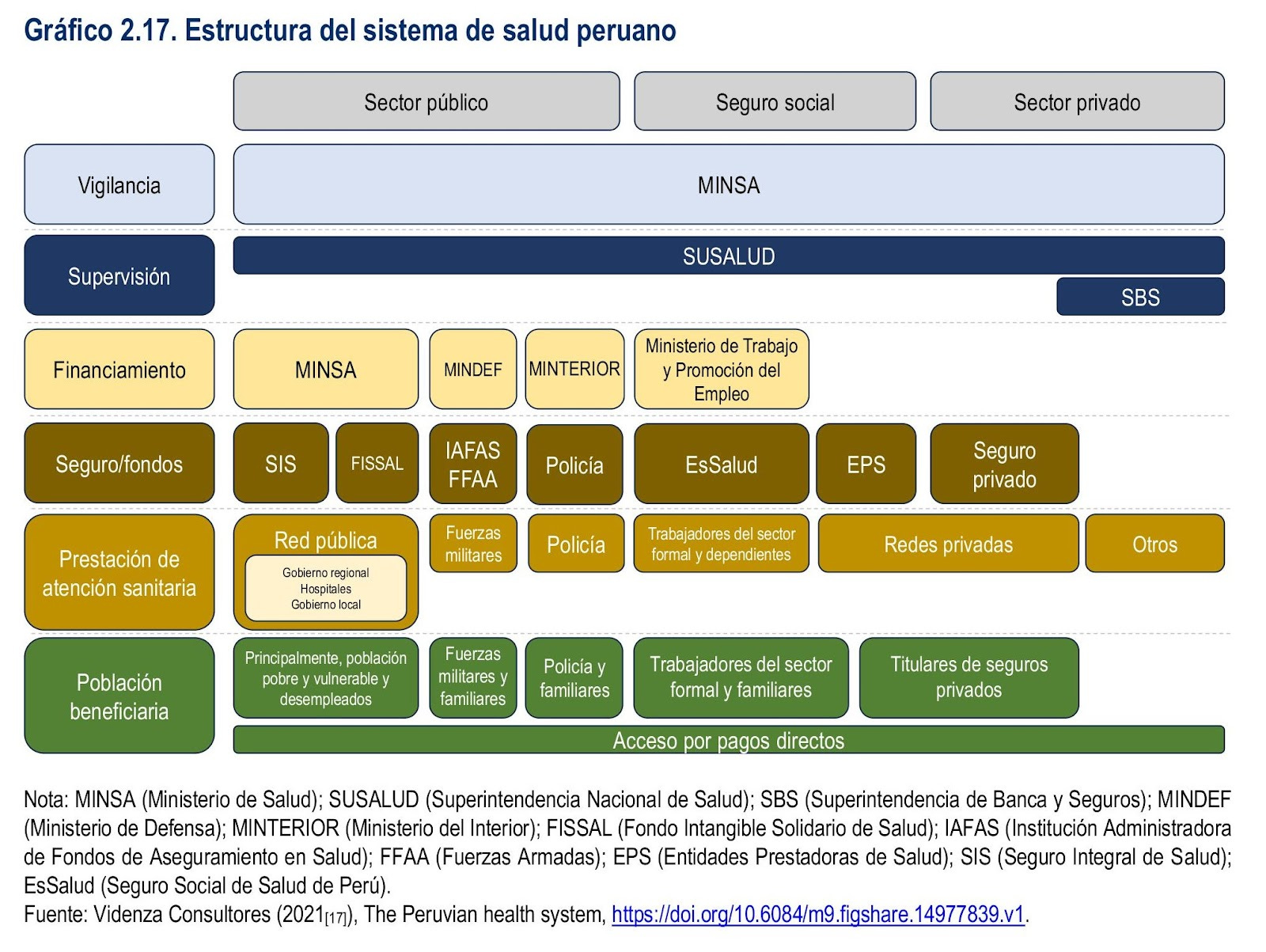

For a better view of the full system, check out the diagram structured by the Organisation for Economic Co-operation and Development (OECD):

Through this model, the country has managed to expand its healthcare coverage, going from 61% of the population in 2009 to 97% in 2023. In this regard, SIS is one of the main players in expanding access to underserved populations.

Even so, the system as a whole still faces limitations due to its low level of integration, service duplication, and lack of interoperability. As a result, only 24% of Peruvians are satisfied with the quality of care and medical services in the country, according to the survey “Percepciones de los peruanos sobre el sistema de salud” conducted by the Peruvian market research firm IPSOS.

Healthcare Challenges

Although coverage has expanded, satisfaction levels remain low. This reveals important structural challenges. According to analyses by the Institute for Health Technology Assessment (IETSI) and Amnesty International, the Peruvian system remains segmented: multiple subsystems (MINSA/SIS, EsSalud, armed forces/police, and the private sector), each with its own rules, finances, and operators, lead to duplicated structures and inefficiencies.

In practice, this fragmentation intensifies territorial inequalities. That is, the infrastructure and quality of services vary greatly between Lima and rural areas, with precarious care outside urban centers.

In addition, studies by ENAHO and the World Bank indicate that although 99% of the population is enrolled in some form of insurance, around 70% of those who needed care in 2022 were unable to access it — due to delays, lack of coordination between facilities, or unavailability of services outside regular hours.

Overall, the low interoperability between subsystems is one of the most critical issues. Although Peru ranks sixth in Latin America in terms of digital capacity, it still lacks systems capable of integrating data across MINSA, EsSalud, and the private sector, which hinders continuity of care.

As for infrastructure, according to data from MINSA, there is significant variation in the number of hospital beds and care units per 10,000 inhabitants across departments, with Lima being favored over regions such as Puno or Loreto.

There is also underfunding of primary care — considered a cornerstone for efficiency and effectiveness. Although there is a digital transformation agenda in place through 2030, implementation is still limited to pilot projects.

Regarding the direct cost to the patient, according to a World Bank analysis, despite having insurance, many Peruvians resort to out-of-pocket payments: around 7 out of 10 people are unable to access formal care and turn to self-medication or pharmacies without proper supervision.

Rising Health Demands in Peru

The main health demands in Peru include a combination of non-communicable chronic diseases, infectious emergencies — such as whooping cough —, environmental risks from pollutants, and issues related to mental health.

First, nearly half of the population over the age of 15 lives with chronic illnesses — including hypertension, diabetes, obesity, arthritis, heart conditions, and cancer — with a 44% prevalence in urban areas compared to 37% in rural areas. Additionally, 42% of adults report having multiple comorbidities.

In terms of mental health, 46% of the population identifies anxiety and depression as major current concerns, compared to the 45% average across Latin America, according to a global survey by IPSOS. Along those lines, the Peruvian Ministry of Health recorded more than 900,000 cases of anxiety and depression between January and June 2024, continuing an upward trend.

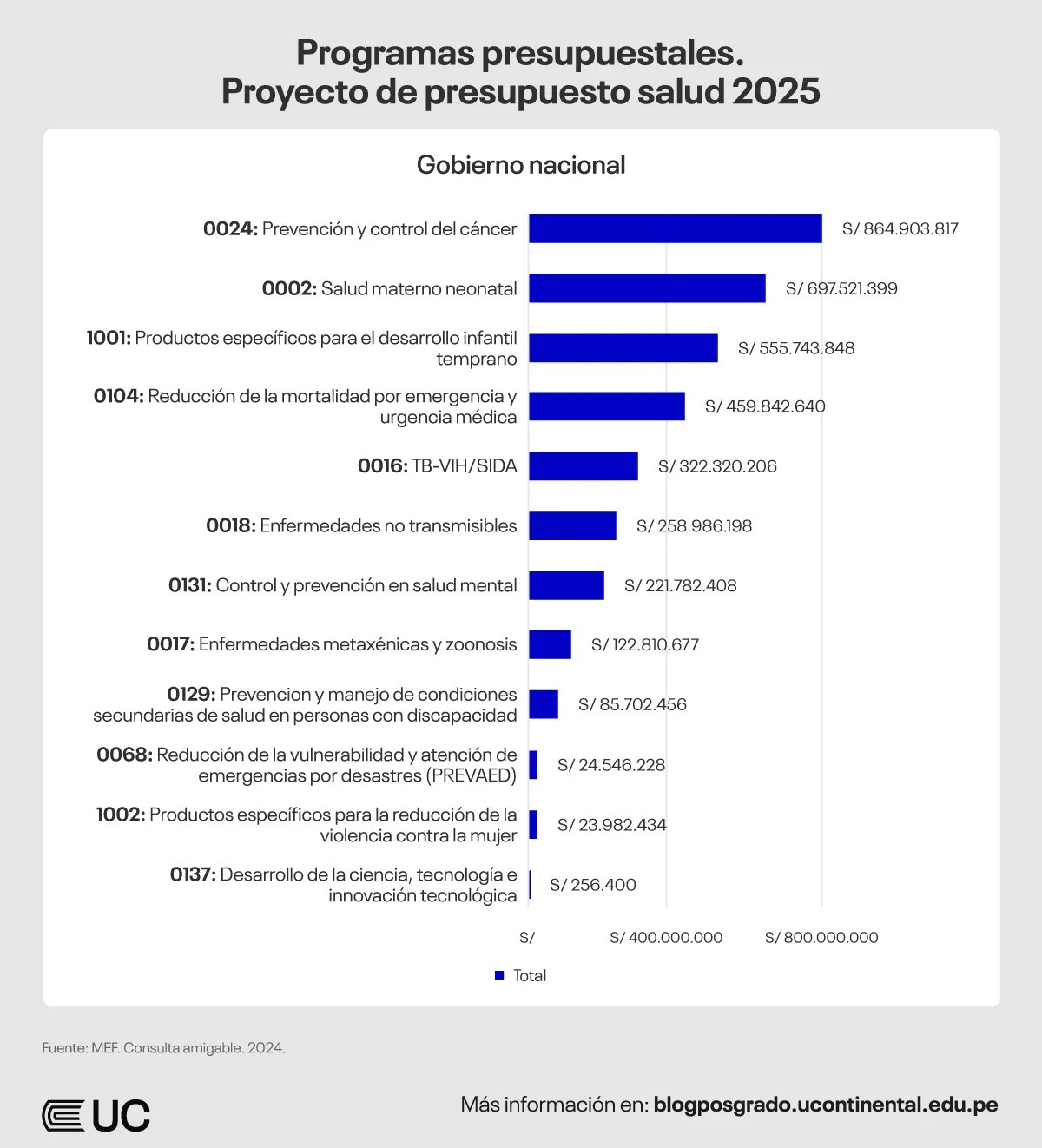

With the increased allocated budget, the Peruvian government is expected to direct investments toward specific areas of the healthcare sector, such as cancer prevention and control, maternal health, child development, emergency care, and others. See the image below:

Private Healthcare Market in Peru

To better understand the current status of private healthcare in Peru, here are some figures reported by the local newspaper Gestión.

In summary, the private healthcare sector generates S/4.6 billion annually (approximately R$7.06 billion) and has shown continuous and sustained growth over the past few years. This scenario is driven by technological, cultural, and emerging demand factors.

According to data from the Peruvian consulting firm Total Market Solutions (TMS), the sector has maintained an average annual growth rate of 9%, with an even higher growth of 10% between 2022 and 2024. Furthermore, according to the 2025 TMS Health Monitor, the year-over-year revenue variation in the private healthcare sector (clinics) was:

- +22.6% (growth) – 2021 vs. 2020

- -3.8% (decline) – 2022 vs. 2021

- +10.9% (growth) – 2023 vs. 2022

- +10.2% (growth) – 2024 vs. 2023

In line with this performance, the TMS Monitor also identified rapid growth in health plans, insurance companies, service providers, and other related entities.

To achieve these results, 15 business groups dominate most of the market, with a particular emphasis on clinical networks. Even so, there are three major groups leading the sector, alongside six mid-sized groups and another six small private operators.

In this context, the years 2023 and 2024 were significant for the consolidation of many of these groups, which opened new facilities and expanded existing ones. TMS analysts expect three new groups to enter the market by the end of 2025.

The positive outlook for the private sector — both in terms of consolidation and future growth — is linked to trend shifts driven by the entry of foreign capital. Among other changes, there have been improvements in technology (such as CT scans and MRIs), infrastructure, and the advancement of decentralized service delivery — which, until now, has remained largely concentrated in Lima, the nation’s capital.

Finally, the consulting firm also highlighted the variation in demand for medical consultations by specialty over the years. These data are also presented in a table published by the newspaper Gestión, based on information from TMS.

Therefore, the healthcare landscape in Peru is characterized by progress in coverage, growth in the private sector, and increasing investments, but it still faces structural barriers that hinder the system’s equity and efficiency.